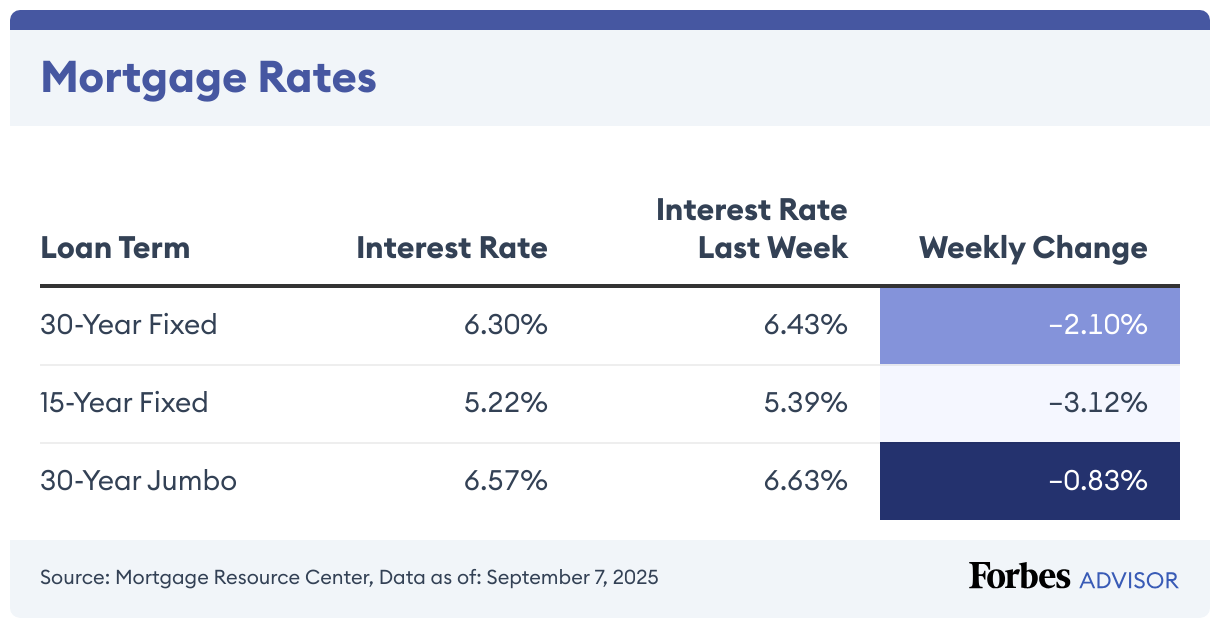

Currently, the average interest rate on a 30-year fixed mortgage is 6.17%, compared to 6.12% a week ago, according to the Mortgage Research Center.

For borrowers who want to pay off their home faster, the average rate on a 15-year fixed mortgage is 5.31%, up 0.26% from the previous week.

If you’re thinking about refinancing to lock in a lower rate, compare your existing mortgage rate with current market rates to make sure it’s worth the cost to refinance.

30-Year Mortgage Rates Climb 0.87%

Today, the average rate on a 30-year mortgage is 6.17%, compared to last week when it was 6.12%.

The APR on a 30-year, fixed-rate mortgage is 6.2%. The APR was 6.15% last week. APR is the all-in cost of your loan.

With today’s interest rate of 6.17%, a 30-year fixed mortgage of $100,000 costs approximately $611 per month in principal and interest (taxes and fees not included), the Forbes Advisor mortgage calculator shows. Borrowers will pay about $120,582 in total interest over the life of the loan.

15-Year Mortgage Rates Climb 0.26%

Today’s 15-year mortgage (fixed-rate) is 5.31%, up 0.26% from the previous week. The same time last week, the 15-year, fixed-rate mortgage was at 5.3%.

The APR on a 15-year fixed is 5.36%. It was 5.35% a week earlier.

A 15-year, fixed-rate mortgage with today’s interest rate of 5.31% will cost $807 per month in principal and interest on a $100,000 mortgage (not including taxes and insurance). In this scenario, borrowers would pay approximately $45,760 in total interest.

Jumbo Mortgage Rates Climb 3.77%

The current average interest rate on a 30-year, fixed-rate jumbo mortgage (a mortgage above 2025’s conforming loan limit of $806,500 in most areas) is 6.63%—3.77% higher than last week.

A 30-year jumbo mortgage at today’s fixed interest rate of 6.63% will cost you $641 per month in principal and interest per $100,000. That adds up to roughly $130,988 in total interest over the life of the loan.

Mortgage Rate Trends in 2025

After reaching 7.04% in January, the average interest rate for a 30-year fixed mortgage has steadily remained in the mid-to-high 6% range. The 15-year fixed mortgage rate has hovered between the low-6% and mid-to-high 5% range since its January peak of 6.27%.

Rates have trended downward since mid-January 2025, but experts aren’t forecasting further significant decreases in 2025. Rate drops may continue in 2026, especially if the Federal Reserve continues to cut the federal funds rate down.

!function(){“use strict”;window.addEventListener(“message”,function(a){if(void 0!==a.data[“datawrapper-height”]){var e=document.querySelectorAll(“iframe”);for(var t in a.data[“datawrapper-height”])for(var r,i=0;r=e[i];i++)if(r.contentWindow===a.source){var d=a.data[“datawrapper-height”][t]+”px”;r.style.height=d}}})}();

When Will Mortgage Rates Go Down?

Various economic factors influence mortgage rates, making it challenging to forecast when rates will drop.

The Federal Reserve’s decisions significantly impact mortgage rates. In response to inflation or an economic downturn, the Fed may lower its federal funds rate, prompting lenders to reduce mortgage rates.

Mortgage rates also track U.S. Treasury bond yields. If bond yields drop, mortgage rates typically follow suit.

Finally, global events that cause financial disruptions can affect mortgage rates. For example, the Covid-19 pandemic led to record-low interest rates when the Fed cut rates.

While a significant decrease in mortgage rates is unlikely in the near future, they may start to decline if inflation eases or the economy weakens.

How To Calculate Mortgage Payments

One of the first steps in buying a house is budgeting. To get a rough idea of how much owning a home will cost, start by using a mortgage calculator to crunch the numbers.

Just input the following data to get an idea of how much a house will cost:

- Home price

- Down payment amount

- Interest rate

- Loan term

- Taxes, insurance and any HOA fees

Find the Best Mortgage Lenders

How Are Mortgage Rates Determined?

Home loan borrowers can qualify for better mortgage rates by having good or excellent credit, maintaining a low debt-to-income (DTI) ratio and pursuing loan programs that don’t charge mortgage insurance premiums or similar ongoing charges that increase the loan’s APR.

Comparing rates from different mortgage lenders is an excellent starting point. You may also compare conventional, first-time homebuyer and government-backed programs like FHA and VA loans, which have different rates and fees.

Several economic factors influence the trajectory of rates for new home loans. For example, Federal Reserve rate hikes indirectly cause the interest rates for many long-term loans to increase. Rates are more likely to decrease when the Fed pauses or decreases its benchmark Federal Funds Rate.

The inflation rate and the general state of the economy also impact interest rates. High inflation and a strong economy typically signal higher rates. Cooling consumer demand or inflation may lead to rate decreases.

Find the Best Mortgage Lenders

Frequently Asked Questions (FAQs)

What is a good mortgage rate?

Average 30-year fixed mortgage rates land in the mid-6% range, so any rate at or below this range would be considered a good rate. However, several factors impact mortgage rates, including the repayment term, loan type and borrower’s credit score, so if you are considering applying for a mortgage, it’s a good idea to compare rates from several lenders to find the best rate for your situation.

How often do mortgage rates change?

Lenders adjust mortgage rates daily based on economic conditions, inflation, bond market movements and Federal Reserve actions.

If you’re shopping around for a mortgage, remember that you might be able to lock in a rate for 30 up to 120 days, depending on the lender. Note that some lenders charge a fee to lock your rate while others offer the service for free.

Should I choose a fixed- or adjustable-rate mortgage?

Choosing between a fixed- or adjustable-rate mortgage (ARM) depends on your financial situation. A fixed-rate mortgage suits those who want consistent monthly payments throughout the loan term without worrying about fluctuations in their rate or payments in response to market changes. If mortgage rates are low, securing a fixed rate can save you money in the long run.

An ARM, on the other hand, may appeal to those who want a lower initial rate and monthly payment. However, you also run the risk of ending up with higher payments if your rate fluctuates. If you expect your income to rise, you may feel confident handling these potential payment increases. These mortgages can also work well for those who plan to live in a home for only a few years, as you might sell or move before the rate adjusts.

Leave a Reply